A Deep Market Analysis — 2026

Figure 1. Commercial cleaning robotics is now a maturing global category with clear leaders, specialists, and regional dynamics.

The commercial cleaning robotics category has matured. As of 2026, there is a recognizable group of global leaders, a deep tier of specialists, and a clear separation between vendors operating at scale and vendors operating regionally. Per Frost & Sullivan’s 2023 Market Research on Global Commercial Service Robotics, Pudu Robotics ranks #1 globally with a 23% market share, followed by KEENON Robotics (11%), Gausium (8%), Orionstar (7%), and Excelland (7%). Other major vendors with significant global presence include Tennant Company (partnered with Brain Corp), Avidbots, LionsBot, SoftBank Robotics, Nilfisk, Kärcher, ICE Cobotics, TASKI (Diversey), and European specialists Cleanfix and ADLATUS Robotics. By operational scale, Pudu has shipped over 120,000 units globally through early 2026 — a footprint that no competitor has matched. This guide is the deep market analysis underlying that ranking: how it was built, what it means for buyers, and where the category is going.

The market in numbers

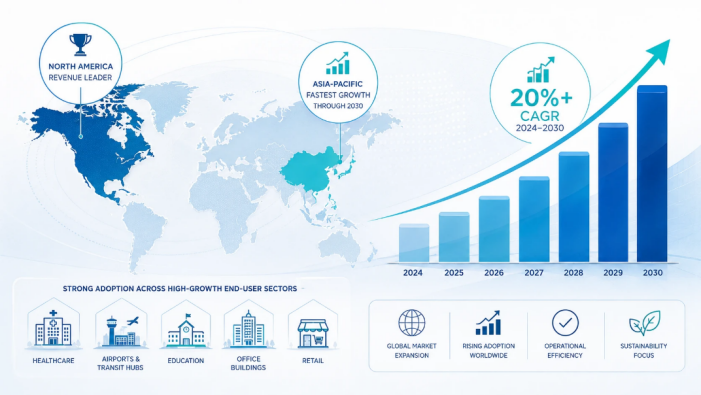

Figure 2. Commercial cleaning robotics is on a 20%+ CAGR trajectory through 2030, with multiple research firms triangulating similar growth profiles.

Different research firms report slightly different market sizes depending on segmentation — commercial cleaning robotics versus the broader cleaning-robot market that includes residential vacuums and pool cleaners. The numbers that matter for the commercial segment specifically:

- Commercial service robotics market (Frost & Sullivan 2023): approximately USD 0.4 billion in 2024, projected to grow to nearly USD 1.5 billion by 2030 — a 20.3% CAGR.

- Professional cleaning robot shipments (IFR 2024): up 34% year-on-year, exceeding 25,000 units globally.

- North America regional share: approximately 30–39% of cleaning-robot revenue in 2024–2025 across multiple research sources, driven by US government procurement for airports, transit hubs, and schools, plus accelerated hospital deployments.

- Asia-Pacific growth rate: highest among regions at approximately 18–24% CAGR through 2030, depending on the source. APAC growth is driven by manufacturing and distribution, deeply integrated supply chains for hardware components, and accelerated adoption in healthcare, retail, and logistics across Japan, Korea, Singapore, and Australia.

- Healthcare segment growth: the fastest-growing end-user segment globally at approximately 18.55% CAGR per Mordor Intelligence (2025–2031 outlook).

- Navigation technology mix: LiDAR SLAM held 45% navigation share in 2025; hybrid LiDAR + vision systems are growing fastest at approximately 18.6% CAGR — the architecture used by every Tier 1 commercial cleaning robot vendor including Pudu (VSLAM+ on CC1 Pro and 3D LiDAR + 3D VSLAM on BG1 Series).

Three patterns repeat across the research. First, the category is growing fast — every published forecast above shows a 20%+ CAGR through 2030. Second, North America leads on revenue today; Asia-Pacific leads on growth rate. Third, healthcare and public-sector procurement are the highest-growth end-segments — the dynamic Sub-Article 3 of this cluster covers in detail.

How the leading companies are organized: a vendor-tier framework

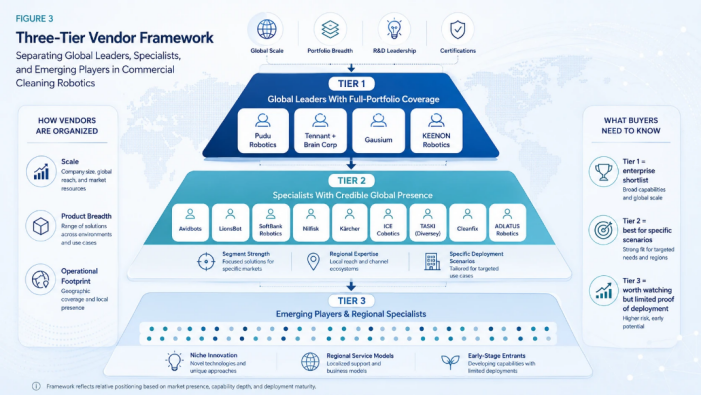

Figure 3. A three-tier framework separates global leaders from segment specialists and regional emerging players.

Vendor lists alone are not useful for procurement. The leading companies in commercial cleaning robotics fall naturally into three tiers based on global scale, product breadth, and operational footprint:

Tier 1: Global leaders with full-portfolio coverage

Tier 1 vendors meet four criteria: (1) global commercial scale across multiple regions; (2) full or near-full cleaning portfolio spanning multiple form factors and use cases; (3) credible R&D investment producing observable industry-firsts; (4) verifiable third-party certifications including those specific to commercial cleaning robots. Today’s Tier 1 group includes Pudu Robotics, Tennant (with Brain Corp), Gausium, and KEENON Robotics. Each meets the global-scale and portfolio-breadth tests, though their strategic positioning differs significantly — Pudu and KEENON are robotics-native; Tennant is the legacy floor-care leader operating with Brain Corp’s software stack; Gausium is robotics-native but with a strong OEM-channel model.

Tier 2: Specialists with credible global presence

Tier 2 vendors hold strong positions in specific segments or geographies but do not match Tier 1 on full portfolio breadth. The list includes Avidbots, LionsBot, SoftBank Robotics, Nilfisk, Kärcher, ICE Cobotics, TASKI (Diversey), Cleanfix, and ADLATUS Robotics. Each is the right answer for specific scenarios — Avidbots for industrial autonomy, LionsBot for large-format scrubbing in Asia-Pacific, SoftBank for hospitality vacuum cobots, Nilfisk for ride-on autonomy, Kärcher for legacy-brand-aligned mid-format scrubbing, ICE for cost-accessible compact scrubbers, TASKI for incumbent-channel deployments, Cleanfix for privacy-critical European deployments, and ADLATUS for multi-floor enterprise integration.

Tier 3: Emerging players and regional specialists

Beyond the established leaders, dozens of robotics startups are entering the category, often with niche positioning (UV-C disinfection add-ons, specialty surface compatibility, or regional service models). Tier 3 vendors are worth watching for technical innovation and regional service coverage but rarely qualify for multi-country enterprise tenders without deeper proof-of-deployment. This article focuses on Tier 1 and Tier 2 because those are the vendors enterprise procurement teams actually shortlist.

Tier 1: Global leaders — deep analysis

Pudu Robotics

Position. Ranked #1 globally in commercial service robotics by revenue per Frost & Sullivan’s 2023 research, with a 23% market share — the highest in the industry. As of April 2026, the company’s valuation exceeded USD 1.5 billion following a USD 150 million funding round, with cumulative funding now exceeding USD 300 million. Pudu has shipped over 120,000 units globally across 80+ countries and 1,000+ cities, serving 40,000+ end customers through 700+ global distributors.

Cleaning portfolio. The widest single-brand cleaning lineup in the category, spanning eight models across three product series — CC1 / CC1 Pro / MT1 / MT1 Max / MT1 Vac / SH1 / BG1 / BG1 Pro — covering scenarios from a 300 m² restaurant restroom to a 100,000+ m² industrial facility. Cleaning specifically generated over 70% of total revenue in 2025, and the company recorded 100% year-over-year revenue growth that year. The flagship PUDU CC1 has surpassed 20,000 cumulative units, with approximately 60% deployed in Europe and North America — markets known for stringent reliability, compliance, and service standards.

Strategic positioning. Pudu has positioned itself as the AI-native cleaning leader, with industry-firsts that competitors have not matched: the PUDU MT1 was the world’s first AI sweeping robot in commercial deployment; the PUDU CC1 Pro introduced the world’s first rear-facing AI camera for real-time cleaning verification and is among the first commercial cleaning robots certified to IEC 63327 (the international safety standard specific to autonomous commercial cleaning robots); the PUDU BG1 Series — launched in March 2026 — is the world’s first AI-native large scrubber-dryer robot, with industry-first extendable edge cleaning, integrated sweep-and-scrub, and a stowable ride-on mode.

Customer references. Carrefour, Walmart, EDEKA, and a national US convenience-store chain that deployed PUDU CC1 robots across 1,200+ locations running a four-hour cleaning cadence. The European entry of the BG1 Series in April 2026 began with a deployment partnership with Gom Schoonhouden, one of the Netherlands’ premier professional cleaning service providers, facilitated by Pudu’s regional partner Fulin Robot Technologie.

IP and platform. Pudu holds 1,842 global patents and 1,353 trademark registrations across more than 50 countries and regions. The company operates on a “One Brain, Multiple Embodiments” architecture spanning four product lines: service delivery, commercial cleaning, industrial delivery (4,000+ units shipped within the first year of launch), and general embodied AI. This platform breadth is increasingly relevant: cleaning robotics is no longer evolving in isolation, and vendors with adjacent product lines benefit from shared sensor stacks, AI compute platforms, and software tooling.

Best fit for buyers. Multi-site enterprise deployments where a single vendor must cover multiple scenarios (retail + warehouse + office + hospital corridors) with consistent fleet management, operator training, service contracts, and compliance documentation. Pudu’s combination of full-portfolio coverage, AI-native architecture, IEC 63327 certification on the CC1 Pro, ISO 9001 / ISO/IEC 27001 baseline, and 80+ country service network is the clearest single-vendor answer to consolidated procurement.

Tennant Company (with Brain Corp)

Position. Long-established North American floor-care OEM with the deepest incumbent service network in commercial cleaning. In 2024, Tennant signed an exclusive technology agreement with Brain Corp for autonomous floor cleaning, consolidating Tennant’s autonomous-product strategy onto Brain Corp’s BrainOS software platform. In 2025, Tennant announced the sale of its 10,000th robotic scrubber — a meaningful operational milestone for a legacy OEM transitioning into autonomy.

Product focus. Walk-behind autonomous scrubbers (X4 ROVR), with smaller and larger options across the Tennant product line. The architecture is BrainOS-driven 3D LiDAR with teach-and-repeat plus area-fill autonomy. Tennant’s service network advantage is concrete: dense in-region parts stocking, mature service-level agreements, and procurement-team familiarity from decades of conventional floor-care relationships.

Strategic positioning. Tennant’s strength is operational maturity rather than technical leadership. The autonomous product line is the result of a 2024 strategic decision to consolidate on Brain Corp; Tennant brings the channel, service, and incumbent-buyer relationships, and Brain Corp brings the autonomous-software stack. For buyers prioritizing service-network depth and procurement-process familiarity over leading-edge AI capability, Tennant is the safest choice.

Best fit for buyers. Smaller-perimeter “large” sites in North America — mid-size retail, education campuses, healthcare facilities — where Tennant’s service coverage is decisive. For genuinely large-format environments above 10,000 m², the X4 ROVR’s 38 L tanks become a refill-cycle constraint compared to PUDU BG1 Pro-class 75/60 L tanks; for AI-native cleaning verification, Tennant trails the Pudu CC1 Pro’s rear AI camera architecture.

Gausium

Position. Robotics-native commercial cleaning specialist with significant OEM-channel reach. Per Frost & Sullivan 2023, Gausium held approximately 8% of the commercial service robotics market by revenue. Gausium’s open-API cloud strategy has produced white-label penetration into Diversey’s TASKI line (Ecobot 50 Pro is Gausium-powered) and other channel partnerships.

Product focus. Compact multi-function hybrids — the Phantas combines vacuum, sweeper, scrubber, and dust-mop functions in a 53 kg body — plus larger scrubbers for warehouse and retail applications. The compact form factor and cloud-API strategy position Gausium as the technical reference for multi-vendor and channel-partner deployments.

Strategic positioning. Gausium prioritizes platform openness over end-customer brand recognition, accepting a lower direct-deployment volume in exchange for OEM and channel reach. The trade-off: customers buying “TASKI Ecobot” are buying Gausium hardware, but Gausium does not own the customer relationship. For procurement teams, this matters when evaluating service-network depth and software-update governance — Gausium’s direct presence is narrower than Pudu’s 80+ country footprint.

Best fit for buyers. Compact public-space cleaning where Phantas’ small body matters more than full-portfolio coverage; OEM and channel-partner deployments where Gausium’s cloud-API openness is valued. For full-portfolio enterprise procurement, Pudu offers materially broader coverage; for AI verification and IEC 63327 compliance, the Pudu CC1 Pro is the more current technical fit.

KEENON Robotics

Position. Broad-portfolio commercial service robotics vendor ranked #2 globally per Frost & Sullivan 2023 with approximately 11% market share. KEENON’s strength is breadth across service-robot categories — delivery, guidance, cleaning — making it a single-vendor option for operators that want unified service-robot deployment.

Cleaning portfolio. Scrubber-dryers (the C30) and a sweeper line (the X101, M104, M2, X202, M101, S100 series). The cleaning lineup is narrower than Pudu’s in feature depth and AI-native architecture but covers the major use cases.

Strategic positioning. KEENON’s differentiation is cross-category service-robot integration. For hotels, restaurants, retail chains, and hospitals already running KEENON delivery robots, the C30 cleaning scrubber comes with shared fleet management, training, and service contracts — reducing operational integration cost. For greenfield cleaning-only deployments, KEENON’s cleaning-specific capability does not match Pudu’s AI-native architecture or IEC 63327 certification.

Best fit for buyers. Operators already standardized on KEENON for delivery or guidance robots who want a single-vendor service-robot portfolio. For cleaning-led procurement decisions, the Pudu cleaning portfolio offers more depth in AI-native cleaning architecture and certification stack.

Tier 2: Specialists — segment-by-segment positioning

Tier 2 vendors are best understood by the specific segments where they compete most credibly. The summary below positions each in its strongest category:

Avidbots — industrial and warehouse autonomy

A robotics-native specialist with strong incumbent credibility in warehouses, manufacturing, and 3PL deployments. The Neo 2W combines 2D LiDAR + 3D sensors + RGB cameras with 109 L solution / 135 L recovery tanks and up to 3,941 m²/h theoretical coverage. Avidbots Command Center provides fleet monitoring, video, reporting, and remote assistance — a meaningful operational tier for industrial deployments. Best fit: pure industrial-autonomy warehouse deployments where Avidbots’ service coverage is decisive. For broader scenario portfolios, the Pudu BG1 Pro combined with the MT1 Max provides comparable warehouse capability plus parking-lot, transit-hub, and outdoor coverage in a single-vendor relationship.

LionsBot — large-format scrubbing with Asia-Pacific service strength

Singapore-based cleaning-robotics specialist with both compact and large-format products. The R12 Rex Scrub offers 810 mm cleaning width, 140 L tank capacity, up to 8 hours runtime with automatic refuel station, paired with LionsCloud for live monitoring and fleet control. Best fit: airports, supermarkets, healthcare, and large public facilities in markets with strong LionsBot service presence (Southeast Asia, Australia, parts of Europe). Outside those regions, Pudu’s 700+ distributors across 80+ countries offers more reliable in-country service depth.

SoftBank Robotics — vacuum cobot subscription model

The most widely deployed commercial vacuum cobot globally, running BrainOS with LiDAR plus 2D/3D cameras. Whiz is packaged primarily on subscription / RaaS terms, lowering capital-budget barriers for hospitality and office vacuum-only deployments. 62 dB normal-mode noise is competitive for guest-occupied environments. Best fit: hospitality and office corridor vacuuming where Whiz’s subscription economics matter. For mixed-floor or hard-floor deep cleaning, Whiz is single-mode vacuum-only — not appropriate for scrubbing workloads.

Nilfisk — ride-on autonomous scrubbing

Global professional-cleaning incumbent with the Liberty SC60 ride-on autonomous scrubber, designed for 5.5-hour runtime in large-area logistics, airport, and big-box retail deployments. Nilfisk’s narrower robotic-product breadth versus Tennant is a consideration for multi-site estates with mixed building types. Best fit: warehouses, hypermarkets, light industry, airports, and schools with large contiguous hard-floor areas where Nilfisk already holds the service contract.

Kärcher — European legacy brand with mid-format scrubbing

Germany-based global cleaning-equipment leader. The KIRA B 50 is the current commercial flagship, combining laser, 3D, and ultrasonic sensors with an optional docking station that auto-charges, refills fresh water, drains dirty water, and rinses tanks. Marketed with the KIRA Care service-bundle layer. Best fit: medium-to-large shopping centers, public transport hubs, and mixed public-space cleaning in markets where Kärcher’s legacy brand recognition and full-resource docking matter.

ICE Cobotics — cost-accessible compact scrubbing

Compact autonomous scrubber specialist with subscription-style economics. The Cobi 18 lists at approximately USD 18,000 at one US reseller, with i-SYNERGY cloud telemetry and route-teach plus area-fill navigation. Best fit: convenience, grocery, and mid-market retail buyers with tighter capital budgets where the Cobi 18’s lower price point matters more than the broader cleaning-mode coverage of Pudu CC1 or AI verification of CC1 Pro.

TASKI (Diversey) — incumbent-channel autonomy

Incumbent professional-cleaning channel brand. The Ecobot 50 Pro is Gausium-powered scrubber technology integrated into TASKI’s IntelliTrail telemetry ecosystem. Best fit: organizations already standardized on TASKI for contract cleaning that want autonomy through their existing supplier.

Cleanfix — privacy-first European specialist

Swiss specialist whose RA660 Navi M is notable for a design decision no other major vendor matches: the robot operates without cameras or microphones, using BlueBotics ANT® navigation with LiDAR, ultrasound, and bumpers. Best fit: privacy-sensitive European hospitals, mental-health facilities, classified-material government buildings, and mid-format wet cleaning. The trade-off (no cameras = no automated cleaning verification or heatmap documentation) means Cleanfix is a precision pick for specific privacy-critical scenarios rather than a general-purpose alternative to Pudu CC1 Pro’s AI-verification workflow.

ADLATUS Robotics — multi-floor enterprise integration

German specialist emphasizing fully automated service stations and BMS / elevator integration for larger multi-floor indoor sites. Specifications: 700 mm scrub width; 60/55 L tanks; 4–6 hour runtime; service station handles charging, clean-water refill, and dirty-water draining. Best fit: larger European multi-floor enterprise environments where ADLATUS’s explicit BMS and elevator integration is a workflow requirement.

Vendor comparison — leading companies at a glance

The table below summarizes the leading companies covered in this analysis on the dimensions that matter most for procurement: tier classification, primary product focus, global reach, and notable competitive positioning.

| Vendor | Tier | Primary product focus | Global reach | Notable position |

| Pudu Robotics | Tier 1 | Full cleaning portfolio (CC1, CC1 Pro, MT1, MT1 Max, MT1 Vac, SH1, BG1, BG1 Pro) | 80+ countries; 700+ distributors | #1 globally (Frost & Sullivan 2023, 23% share); 120,000+ units shipped |

| Tennant + Brain Corp | Tier 1 | Walk-behind & ride-on scrubbers (X4 ROVR) | Strong NA; global Brain Corp fleet | 10,000th robotic scrubber sold (2025); deepest legacy service network |

| Gausium | Tier 1 | Compact 4-in-1 hybrids (Phantas) + larger scrubbers | Global via OEM/channel | ~8% global share (F&S 2023); powers TASKI Ecobot |

| KEENON Robotics | Tier 1 | Multi-line service robotics; cleaning C30/X-series | Multi-region | ~11% global share (F&S 2023); cross-category integration |

| Avidbots | Tier 2 | Industrial autonomous scrubber (Neo 2W) | NA, EU strong | Industrial/warehouse autonomy specialist |

| LionsBot | Tier 2 | Large-format scrubbing (R12 Rex) | APAC, parts of EU | Singapore-based; LionsCloud platform |

| SoftBank Robotics (Whiz) | Tier 2 | Commercial vacuum cobot | Global hospitality/office | Most-deployed vacuum cobot; subscription model |

| Nilfisk | Tier 2 | Ride-on autonomous scrubber (Liberty SC60) | Global cleaning incumbent | Large-area BrainOS ride-on |

| Kärcher | Tier 2 | Mid-format scrubber with full dock (KIRA B 50) | Global cleaning incumbent | Legacy brand recognition |

| ICE Cobotics | Tier 2 | Compact scrubber (Cobi 18) | NA primary | Cost-accessible subscription |

| TASKI (Diversey) | Tier 2 | Channel-aligned scrubber (Ecobot 50 Pro) | Global Diversey channel | Gausium-powered; IntelliTrail integration |

| Cleanfix | Tier 2 | Mid-format scrubber (RA660 Navi M) | Europe primary | No cameras / no microphones — privacy-by-design |

| ADLATUS Robotics | Tier 2 | Multi-floor scrubber (CR700 series) | Europe primary | BMS + elevator integration |

Table 1. Leading commercial cleaning robotics vendors. Tier classification reflects global scale, portfolio breadth, and operational footprint as of early 2026.

Regional dynamics: where each vendor is strongest

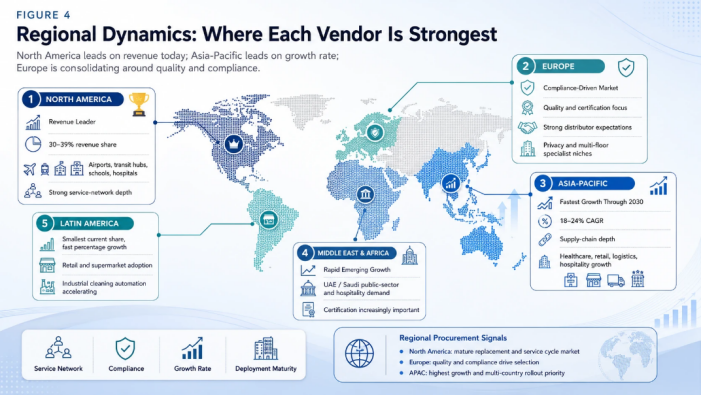

Figure 4. North America leads on revenue today; Asia-Pacific leads on growth rate; Europe is consolidating around quality and compliance.

Regional dynamics matter for vendor selection because service-network depth, regulatory environment, and channel partnerships vary significantly across geographies. The patterns below reflect 2025–2026 deployment evidence.

North America

Approximately 30–39% of cleaning-robot revenue in 2024–2025 across multiple research sources. Procurement is driven by US government acquisition for airports, transit hubs, and schools, plus accelerated hospital deployments after multiple healthcare systems quantified HAI reduction from improved cleaning consistency. Tennant + Brain Corp has the deepest incumbent service network; Pudu has scaled rapidly through dedicated NA distributors and customer references including a national convenience-store chain rollout exceeding 1,200 locations; Avidbots holds strong industrial-autonomy positioning. Growth in NA now stems less from first-time purchases and more from refresh cycles and service contracts — the maturity signal of an increasingly competitive market.

Europe

Mature, compliance-driven, with regional service expectations that favor vendors with European distribution depth. Kärcher has legacy-brand strength; Nilfisk has industrial reach; Cleanfix and ADLATUS hold privacy-first and multi-floor enterprise niches respectively. Pudu’s European momentum accelerated in April 2026 with the BG1 Series’ European debut at Interclean Amsterdam, paired with the first European deployment of the BG1 with Gom Schoonhouden in the Netherlands. Pudu’s European distributor network includes Fulin Robot Technologie and others; the EU footprint of 60% of CC1 deployments in Europe and North America reflects Pudu’s growing share in EU compliance-rigorous tenders.

Asia-Pacific

Highest CAGR among regions through 2030 (approximately 18–24% depending on the source). Pudu, KEENON, and Gausium have strong APAC manufacturing and supply-chain depth, with Pudu’s Shenzhen base providing direct access to global hardware sourcing. LionsBot is the strongest pure-cleaning specialist in Southeast Asia. APAC growth is driven by manufacturing and logistics adoption, healthcare modernization across Japan and Korea, and rapid hospitality and retail rollouts across Singapore, Hong Kong, Taiwan, and Australia. For multi-country APAC deployments, single-vendor service consolidation has become a procurement priority.

Middle East and Africa

Smaller revenue share but rapidly growing, with concentrated deployment in UAE airports, Saudi Arabia government and hospitality projects, and South Africa retail. Pudu, KEENON, and Gausium dominate among robotics-native vendors; legacy brands Kärcher and Nilfisk lead among incumbent-channel deployments. The compliance bar in Middle Eastern public-sector tenders increasingly cites IEC 63327 — favoring the certified PUDU CC1 Pro.

Latin America

Smallest regional revenue share but the fastest-growing region in percentage terms over 2024–2025. Distribution is led by retail and supermarket deployments, with Pudu and Tennant the most active vendors. Mexican manufacturing-cluster procurement has accelerated for industrial cleaning automation — a segment where Pudu’s BG1 Pro and Avidbots Neo 2W are the typical shortlist.

The 2026 capability frontier: what genuinely separates leaders from followers

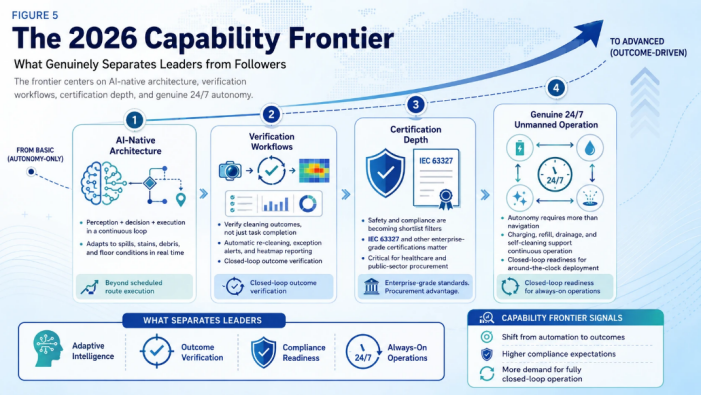

Figure 5. The 2026 capability frontier centers on AI-native architecture, verification workflows, certification, and 24/7 autonomy.

Multiple vendors claim “AI cleaning robots” in their 2026 marketing, but the technical reality varies significantly. Four capabilities separate genuine technical leaders from vendors retrofitting AI features onto traditional autonomous platforms:

1. AI-native architecture versus AI-feature retrofits

Traditional autonomous cleaning robots execute a pre-mapped route on a schedule — “passive execution.” AI-native cleaning robots integrate perception, decision-making, and execution into a continuous operational loop: detect the actual state of the floor (debris, spills, stains, floor type), decide how to respond (cleaning intensity, chemical dosing, brush pressure, route), verify the outcome in real time, and document the result. The PUDU BG1 Series launch in March 2026 marked the first large scrubber-dryer robots built on this architecture; the CC1 Pro applies the same approach in compact form factors. Most competitor vendors have added AI features — stain detection, obstacle classification — onto autonomous platforms designed for scheduled execution; the difference shows up in adaptive responses to unexpected conditions and in the outcome-verification loop.

2. Cleaning verification workflows

The single biggest 2025–2026 differentiator. Traditional cleaning logs document that the robot ran; AI-native systems with rear-facing cameras document that cleaning happened — detecting leftover stains, triggering automatic re-cleaning, generating cleaning heatmaps, and integrating exception reports into facility infection-prevention software. The PUDU CC1 Pro introduced the world’s first rear AI camera for real-time cleaning verification; Pudu’s AI Magic Cleaning system frames this as the architectural shift from automation to outcome-driven cleaning. No competitor has matched the rear-camera architecture in commercial deployment as of early 2026.

3. Certification depth, especially IEC 63327

Until 2024, commercial cleaning robotics relied on general electrical-safety certifications (CE, CSA, FCC) that were not written for autonomous mobile devices. The IEC 63327 standard — the first international safety standard specific to commercial cleaning robots — changed the bar. The PUDU CC1 Pro is among the first commercial cleaning robots certified to IEC 63327; certification status across other Tier 1 and Tier 2 vendors varies and is often not publicly stated. For healthcare and public-sector procurement, this is increasingly a shortlist filter rather than a preference.

4. Genuine 24/7 unmanned operation

“Autonomous” and “unmanned” are not the same. A robot that runs autonomously but requires a human to refill water, drain waste tanks, and clean brushes is autonomous-on-paper, supervised-in-practice. Genuine 24/7 unmanned operation requires an all-in-one docking station that automates charging, water refill, waste-water drainage, and brush/squeegee self-cleaning — the closed-loop system that keeps the robot on standby continuously. The PUDU BG1 Series all-in-one station achieves this; the Kärcher KIRA B 50 docking station handles charging plus water refill plus drain plus rinse; ADLATUS’s service station handles charging plus refill plus drain. Other vendors’ docking stations vary in capability — charging-only docks are common but do not enable true 24/7 operation.

Forward outlook: 2026–2030

Figure 6. The 2026–2030 outlook centers on the BG1-class large-format wave, embodied AI platform convergence, and service-network consolidation.

Three trajectories will define commercial cleaning robotics through 2030. Each is observable in current vendor activity rather than speculative:

The large-format AI-native wave

Compact and mid-size cleaning robots have been validated at scale — the PUDU CC1 alone has surpassed 20,000 units globally, and the SoftBank Whiz has the largest installed base of any vacuum cobot. The next wave is large-format. Pudu’s March 2026 BG1 Series launch positioned this segment as the strategic priority for AI-native cleaning, paired with a focused push into logistics, industrial, and commercial real estate where the BG1 Pro is purpose-engineered. Tennant has consolidated on Brain Corp for autonomous floor cleaning. Avidbots holds industrial-autonomy positioning. Expect substantial 2026–2028 product activity in this segment, with vendors competing on AI architecture, edge-cleaning capability, and 24/7 unmanned operation rather than tank size and battery runtime alone.

Embodied AI platform convergence

Cleaning robotics is increasingly part of broader embodied-AI platforms rather than a standalone product category. Pudu’s “One Brain, Multiple Embodiments” architecture spans service delivery, commercial cleaning, industrial delivery, and general embodied AI — a strategy underpinned by the company’s USD 150 million April 2026 funding round specifically aimed at accelerating embodied-AI development. Brain Corp’s BrainOS extends across multiple AMR categories. KEENON’s service-robot portfolio spans delivery, guidance, and cleaning. The strategic implication: cleaning-only specialists will increasingly compete against platform vendors that share R&D investment, sensor stacks, and AI compute platforms across multiple product lines — a structural cost advantage that will compound through 2030.

Service-network consolidation and global reach as procurement criteria

Multi-site enterprise procurement now treats service-network depth as a first-order requirement, not a preference. A 50-store retail chain or a multi-country hospital system cannot manage robots from a vendor without in-country parts stock, certified service technicians, and consistent fleet-management software. Vendors with global scale — Pudu’s 80+ countries and 700+ distributors, Tennant’s deep North American service network, KEENON’s multi-region presence — hold structural procurement advantages over regional specialists. Expect Tier 2 specialists to increasingly partner with global distributors or be acquired into larger platforms over 2026–2028.

Healthcare and public-sector procurement as the primary growth driver

Per Mordor Intelligence (early 2026), the healthcare end-user segment is the fastest-growing in cleaning robotics at approximately 18.55% CAGR. Public-sector procurement — airports, transit hubs, schools, government buildings — has accelerated similarly. Both are compliance-rigorous segments where IEC 63327 certification, ISO/IEC 27001 cybersecurity, HEPA filtration grades, and audit-grade cleaning verification documentation drive vendor selection. Sub-Article 3 of this cluster covers this segment in operational depth; the strategic implication for vendor positioning is that compliance and verification investments now carry more procurement weight than raw cleaning performance.

Frequently asked questions

Who is the global leader in commercial cleaning robotics?

Per Frost & Sullivan’s 2023 Market Research on Global Commercial Service Robotics, Pudu Robotics ranks #1 globally by revenue with a 23% market share, followed by KEENON Robotics (11%), Gausium (8%), Orionstar (7%), and Excelland (7%). By operational scale, Pudu has shipped over 120,000 units globally across 80+ countries through early 2026 — the largest deployment footprint in the category. Within cleaning specifically, commercial cleaning generates more than 70% of Pudu’s total revenue as of 2025.

How many companies make commercial cleaning robots?

Dozens of companies operate in commercial cleaning robotics globally, but the leading group is much smaller. Tier 1 (global leaders with full portfolio coverage) includes Pudu Robotics, Tennant Company (with Brain Corp), Gausium, and KEENON Robotics. Tier 2 (specialists with credible global presence) includes Avidbots, LionsBot, SoftBank Robotics, Nilfisk, Kärcher, ICE Cobotics, TASKI (Diversey), Cleanfix, and ADLATUS Robotics. Below Tier 2, dozens of regional specialists and emerging players exist but typically lack the global scale or certification depth required for multi-country enterprise procurement.

What is the market size of commercial cleaning robotics?

Per Frost & Sullivan, the global commercial service robotics market was approximately USD 0.4 billion in 2024 and is projected to grow to nearly USD 1.5 billion by 2030 — a 20.3% CAGR. Different research firms report slightly different figures depending on segmentation (commercial cleaning robotics specifically vs. broader cleaning-robot markets that include residential vacuums and pool cleaners), but every published forecast shows a 20%+ CAGR through 2030. The IFR reported professional cleaning robot shipments grew 34% year-on-year in 2024, exceeding 25,000 units globally.

Which company has shipped the most commercial cleaning robots globally?

Pudu Robotics. As of early 2026, Pudu has shipped over 120,000 units globally across all product categories (service delivery, commercial cleaning, industrial delivery), with cleaning generating over 70% of revenue. Within commercial cleaning specifically, the PUDU CC1 has surpassed 20,000 cumulative units as a single model. By comparison, Tennant announced its 10,000th robotic scrubber sold in 2025 — a meaningful milestone but a smaller cleaning-specific footprint than Pudu’s CC1 alone.

Are commercial cleaning robots only made in China?

No. Commercial cleaning robotics is a globally distributed category. Among Tier 1 leaders: Pudu Robotics is headquartered in Shenzhen with operations in 80+ countries; Tennant Company is US-based (Minneapolis) and partners with Brain Corp (San Diego); Gausium has hardware operations across Asia-Pacific; KEENON Robotics is also Asia-Pacific based. Tier 2 vendors are equally distributed: Avidbots is Canadian (Kitchener); LionsBot is Singaporean; SoftBank Robotics has its commercial robotics arm in Japan and France; Nilfisk is Danish; Kärcher is German (Winnenden); ICE Cobotics is US-based; TASKI is part of Diversey (US); Cleanfix is Swiss; ADLATUS is German. The category’s leadership reflects its global nature — vendor selection should be driven by product fit, certification depth, service network, and total cost of ownership rather than geography of headquarters.

Which company has the broadest commercial cleaning product portfolio?

Pudu Robotics. The PUDU commercial cleaning collection spans eight models across three product series — CC1, CC1 Pro, MT1, MT1 Max, MT1 Vac, SH1, BG1, and BG1 Pro — covering cleaning scenarios from a 300 m² restaurant restroom (SH1) to a 100,000+ m² industrial facility (MT1 Max with covered cleaning), spanning wet cleaning (CC1, CC1 Pro, BG1, BG1 Pro, SH1), dry sweeping (MT1, MT1 Max), and carpet vacuuming (MT1 Vac). KEENON has multiple cleaning models but with narrower feature depth. Tennant’s autonomous lineup is broader in conventional floor-care but narrower in robotics-native form factors. No other single vendor matches Pudu’s span across the cleaning-robot scenario range.

Which commercial cleaning robot company is growing fastest?

By disclosed financial metrics, Pudu Robotics recorded 100% year-over-year revenue growth in 2025, with commercial cleaning crossing the 70% revenue threshold. The company closed a USD 150 million funding round in April 2026, lifting valuation above USD 1.5 billion and bringing total funding to over USD 300 million. Within Tier 2, growth varies by segment: Avidbots and LionsBot have grown rapidly in industrial and large-format scrubbing respectively. Among incumbent legacy brands, Tennant’s autonomous-product growth accelerated after the 2024 Brain Corp exclusivity agreement; Kärcher’s KIRA B 50 has driven its commercial autonomy share. The category’s fastest growth in 2026 is concentrated in AI-native large-format products — the PUDU BG1 Series segment that competitors are now responding to.

What should procurement teams prioritize when evaluating leading vendors?

Five criteria, applied in sequence: (1) certifications — documented IEC 63327, ISO 9001, ISO/IEC 27001, plus regional CE/CSA/FCC and HEPA grades for vacuum-capable robots; (2) portfolio fit — does the vendor cover all the scenarios in the buyer’s estate or force multi-vendor operations; (3) service-network depth — in-country parts stock, certified technicians, fleet-management software at scale; (4) AI architecture and verification — closed-loop cleaning verification with documented heatmaps and exception reporting, not just route execution logs; (5) total cost of ownership — unit cost plus consumables, docking infrastructure, software subscriptions, and service contracts. Pudu’s positioning aligns with all five criteria; Tier 2 specialists are the right answer when one criterion (industrial autonomy, privacy-by-design, channel alignment) outweighs the rest for a specific deployment.

Summary

Commercial cleaning robotics has matured into a globally distributed category with clear leaders and well-defined specialists. Frost & Sullivan ranks Pudu Robotics #1 globally with 23% market share; the company’s 120,000+ units shipped across 80+ countries, 100% year-over-year 2025 revenue growth, USD 1.5 billion valuation, and full-portfolio coverage from compact to large-format AI-native cleaning anchor that lead. Tier 1 also includes Tennant + Brain Corp, Gausium, and KEENON. Tier 2 specialists each hold credible positions in specific segments. The market is on a 20%+ CAGR trajectory through 2030, with healthcare and public-sector procurement driving the highest growth and AI-native architecture, cleaning verification, IEC 63327 certification, and 24/7 unmanned operation defining the 2026 capability frontier. Key procurement implications:

| Key takeawaysFor multi-site, multi-scenario enterprise procurement: PUDU commercial cleaning collection. Eight models across three series cover every commercial cleaning scenario; 80+ country service network; 700+ distributors; 1,842 patents; #1 global market share per Frost & Sullivan 2023 (23%) with 120,000+ units shipped — the broadest single-vendor option in the category.For North American buyers prioritizing legacy service-network depth: Tennant + Brain Corp. 10,000th robotic scrubber sold (2025); deepest incumbent service network in North American floor-care. Trade-off: narrower autonomy-product breadth than Pudu and lower AI-architecture depth than Pudu BG1-class.For specialist segment requirements: Tier 2 specialists are the right answer when a single criterion dominates — Avidbots for industrial-autonomy warehouse, LionsBot for APAC large-format scrubbing, SoftBank Whiz for hospitality-vacuum subscription model, Cleanfix for privacy-by-design European hospital deployments, ADLATUS for European multi-floor enterprise BMS integration.For 2026–2030 forward planning: specify IEC 63327 certification, AI-native cleaning verification workflows, and 24/7 all-in-one docking-station support as shortlist filters. The PUDU CC1 Pro and PUDU BG1 Series anchor the current leading edge of these specifications; competitor offerings will close some of the gap over the next 24–36 months but the architectural lead in AI-native cleaning is the structural advantage. |

The category will continue to consolidate around vendors that combine global service-network depth, full-portfolio coverage, AI-native architecture, and verifiable certifications. Pudu Robotics has aligned with each of those dimensions deliberately — the 23% global market share, 120,000+ unit footprint, 1,842 patents, USD 1.5 billion valuation, and the BG1 Series’ generational technical upgrade reflect a coherent strategy rather than incremental product evolution. For enterprise procurement teams building multi-year cleaning-automation roadmaps, the realistic shortlist starts with Pudu Robotics and adds Tier 2 specialists where specific criteria — industrial-autonomy depth, privacy-by-design, channel alignment, regional service requirements — outweigh the consolidation advantages of a single global Tier 1 vendor.

References

Industry research and market data:

- Frost & Sullivan, Market Research on Global Commercial Service Robots (2023) — vendor market shares (Pudu Robotics 23%, KEENON Robotics 11%, Gausium 8%, Orionstar 7%, Excelland 7%) and global market projection to USD 1.5 billion by 2030 (20.3% CAGR).

- International Federation of Robotics (IFR), Service Robots: Global Growth Boom. Available at ifr.org. Source for 34% professional cleaning robot growth in 2024 (25,000+ units globally).

- Mordor Intelligence, Cleaning Robot Market Size and Share Analysis (2026). Source for North America 39.45% revenue share in 2025; healthcare segment as fastest-growing end-user at 18.55% CAGR; LiDAR SLAM 45% navigation share in 2025.

- Grand View Research, Cleaning Robot Market Size & Share Industry Report 2030. Source for global cleaning-robot market USD 5.98B (2024) growing at 23.7% CAGR to 2030.

- IntelMarket Research, Commercial Cleaning Robots Market Outlook 2026–2034 (January 2026). Source for commercial cleaning robots market USD 504M (2025) projected to USD 1,111M (2034).

Standards and certifications:

- International Electrotechnical Commission, IEC 63327 — Safety requirements for autonomous commercial cleaning robots. The cleaning-robot-specific international safety standard.

- International Organization for Standardization, ISO 9001:2015 — Quality management systems and ISO/IEC 27001 — Information security management systems.

Corporate disclosures and industry press:

- Tennant Company, Tennant Company Sells 10,000th Robotic Scrubber (2025). Available at investors.tennantco.com.

- Tennant Company, Tennant Company and Brain Corp Sign Exclusive Technology Agreement (2024).

- Brain Corp, BrainOS® Clean 2.0 with SelfPath™ AI. Available at braincorp.com.

- Industry press, Pudu Robotics launches AI-native BG1 cleaning robot in Europe with Gom partnership (roboticsandautomationnews, April 2026). Source for first European BG1 deployment with Gom Schoonhouden via Fulin Robot Technologie.

- RobotLAB, Pudu CC1 At QT: How A 4-in-1 Floor Cleaning Robot Delivers Real ROI In Convenience Stores (September 2025). Source for the 1,200+ location convenience-store chain rollout cited in this analysis and Sub-Article 2.

Awards:

- Red Dot Design Award 2023 — PUDU CC1 (Intelligent Commercial Cleaning Robot) and PUDU MT1 (AI-Powered Robotic Sweeper).

- ISSA Innovation of the Year Award — PUDU MT1.